Retirement Planning Clonmel

I’m approaching retirement, what are my financial options?

|

The months leading up to your retirement are a busy time as you make plans to secure your financial future. One of the most important decisions you will make during this time is what to do with your retirement fund once you retire.

You have a number of options available to you. You will usually be able to take part of your retirement fund as a lump sum. Some, or all of this lump sum, may be taken tax-free. Then, provided you meet certain criteria, you can use the remainder in a number of ways. |

Once you meet certain criteria, you can use the remainder of your retirement fund in the following ways:

- Buy an Annuity – a regular guaranteed income for the rest of your life

- Re-invest it in an Approved Retirement Fund (ARF) and/or an Approved Minimum Retirement Fund (AMRF)

- Take as a Taxable Cash Lump Sum subject to PAYE.

Why would I need to use a Financial Broker?

|

Choosing the right option for your retirement can be a daunting task. Your Financial Broker will be able to explain the choices available to you in simple language, allowing you to make an informed decision.

read more

Your Financial Broker will get to know you, your personal and financial circumstances, retirement plans and your attitude to and capacity for risk – products like ARFs for example, contain a certain level of risk that you need to be aware of. Your Financial Broker will guide you through the process of setting up your ARF or annuity and help you to make sense of charges, tax obligations and rates. They will advise and assist you in developing a well researched and structured investment strategy for your ARF that is compatible with your attitude to and capacity for risk and is designed to achieve your goals as far as possible. Ultimately, your Financial Broker will ensure you choose the product best suited to you. |

Retirement Planning

What is an ARF?

|

An ARF is a flexible investment fund that you own personally and can manage and control during retirement. With an ARF you can invest the balance of your retirement fund, after you have taken your lump sum at retirement, in a wide range of different investment funds.

You can also make withdrawals from your ARF as you need to (you must withdraw a minimum of 4% of your fund each year from the year you first reach 61. The minimum withdrawal will increase to 5% from the year you reach 71.). And because you own your fund, you can leave the balance to your dependants when you die. |

Before you invest in an ARF, you must meet one of the following conditions:

- You must be in receipt of a guaranteed pension income payable for life of at least €12,700 a year.

- You must already have invested at least €63,500 of your retirement funds in an ARF or in the purchase of an annuity.

What retirement arrangements are eligible for the ARF option?

read more

Your Financial Broker will advise you about the types of retirement arrangement from which funds can be transferred to an ARF and/or AMRF at retirement. The eligible arrangements are:

• Personal Retirement Savings Accounts (PRSAs).

• Personal Pension Plans.

• Employer defined contribution occupational pension schemes, whose rules

provide the ARF option to retirees. (The option does not apply to Defined

Benefit (DB) arrangements.)

• Buy-Out Bonds, where the bond was funded by a transfer value from a defined

contribution occupational pension scheme.

• Existing ARFs – you can transfer from one ARF to another.

• AVCs (additional voluntary contributions) and PRSA AVCs.

• Personal Retirement Savings Accounts (PRSAs).

• Personal Pension Plans.

• Employer defined contribution occupational pension schemes, whose rules

provide the ARF option to retirees. (The option does not apply to Defined

Benefit (DB) arrangements.)

• Buy-Out Bonds, where the bond was funded by a transfer value from a defined

contribution occupational pension scheme.

• Existing ARFs – you can transfer from one ARF to another.

• AVCs (additional voluntary contributions) and PRSA AVCs.

What are the withdrawal options for ARFs?

read more

|

You will be able to take regular and occasional withdrawals from your ARF at any time. However, if you are aged 61 or over in a year, you are required to withdraw a minimum of 4% of your fund each year. This amount will increase to 5% from the year you reach 71. If the total value of your ARFs and Vested PRSAs is more than €2,000,000 then you are required to withdraw a minimum of 6% from the year you reach 61. Most ARF product providers will pay the minimum withdrawal out to you if you are aged 61 or over in that year, unless you request otherwise.

It’s important to note that regular withdrawals may not be payable for life. the value of your fund can fall as well as rise, and the withdrawals you take could reduce your fund quicker than expected if investment market conditions are poor. It is possible that your ARF fund could run out of capital, and hence regular income, before you die. A withdrawal from an ARF will be subject to income tax, PRSI (up to age 66) and the Universal Social Charge (USC). |

What are the withdrawal options for AMRFs?

read more

Withdrawals from AMRFs will be limited to 4% of the value of the fund each year. No other withdrawals are allowed from your AMRF until you can prove that you are in receipt of a guaranteed pension of €12,700 a year, or until your 75th birthday (at which point your AMRF becomes an ARF).

In making withdrawals from your ARF, you should remember the following points:

In making withdrawals from your ARF, you should remember the following points:

- Making regular withdrawals may reduce the value of your ARF, especially if investment returns are poor or you choose a high rate of withdrawal.

- Regular withdrawals over a long period of time could use up all of your ARF before you die, if your ARF grows at a slower rate than the rate of withdrawal.

- The higher the level of regular withdrawals you make, the higher the chances are that you will use up your ARF in your lifetime.

- If your ARF fund will provide your only, or main, source of income after you retire, you should consider investing some or all of it in an annuity in order to have a guaranteed income for life.

What are the advantages and disadvantages of an ARF?

With any financial product, there are pros and cons. We’ve listed below the main advantages and disadvantages of an ARF, all of which your Financial Broker will be able to explain to you in more detail.

Advantages

- You are in control of your retirement fund. This could be a key factor if you are in poor health or you want to leave the balance of your fund to your dependants after you die

- You decide when and at what rate you draw on your ARF in retirement (subject to a minimum 5% per year withdrawal from the age of 61).

- You decide when and at what rate you draw on your ARF in retirement (subject to the minimum withdrawal amount).

- Any investment growth achieved on your ARF is tax-free; however, withdrawals from your ARF are taxable.

- If you decide that you need a secure, regular income your ARF can be used to buy an annuity at a later date. By waiting, you may be able to get a higher annuity rate for the same lump sum, as you will be older.

- Annuity rates are at historically low levels currently, so ARFs will enable you to defer the purchase if you believe rates will improve in the future.

Disadvantages

- There is no guarantee that your ARF will keep its value; the assets in which your ARF invests may not perform as well as expected and could fall in value.

- Your ARF could run out in your lifetime. This could happen for a number of reasons: you take income from your ARF at too high a rate, your ARF’s investment return is less than expected, and/or you live longer than expected.

- Some ARFs have high on-going charges which reduce the value of your fund.

- If you do decide to use your ARF to buy an annuity later on, there is no guarantee you will be able to get a higher annuity rate than available today.

- You may have to pay for any ongoing investment advice about your ARF.

What are the main differences between an ARF and an annuity?

read more

The key differences between an ARF and an annuity are flexibility and risk. An annuity converts the money in your retirement fund into a guaranteed taxable income payable for your lifetime, fixed on the date you buy the annuity. However on death, there may be little or no return for your dependants.

An ARF allows you to preserve, manage and control your retirement fund. You can invest your money into suitable assets and decide how much taxable income you want to withdraw each year, subject to the minimum withdrawal once you are aged

61 or over. It does not provide any guaranteed income but any balance in your ARF on death is payable to your dependants.

Annuity

ARF

An ARF allows you to preserve, manage and control your retirement fund. You can invest your money into suitable assets and decide how much taxable income you want to withdraw each year, subject to the minimum withdrawal once you are aged

61 or over. It does not provide any guaranteed income but any balance in your ARF on death is payable to your dependants.

Annuity

- Offers an income guaranteed payable for life.

- There is no flexibility and no ability to make changes to your annual income, once you purchase the annuity.

- You are locked into a set annuity rate, fixed on the date of investment, with no potential for growth.

- Income stops when you and your partner (if you have a joint life annuity) die; there is likely to be little or no payment to your dependants on death.

ARF

- Your fund could run out during your lifetime, leaving you with no regular income.

- Your ARF does not provide a guaranteed income for life unless it invests in an annuity.

- You can decide how much money you withdraw each year. (You must normally withdraw a minimum amount each year).

- Your fund can be invested into suitable assets, which means you can benefit from potential growth in that investment.

- However, it is also possible that the value of your fund could drop, depending on your investment options.

- You can leave any remaining funds (subject to tax) to your dependants when you die.

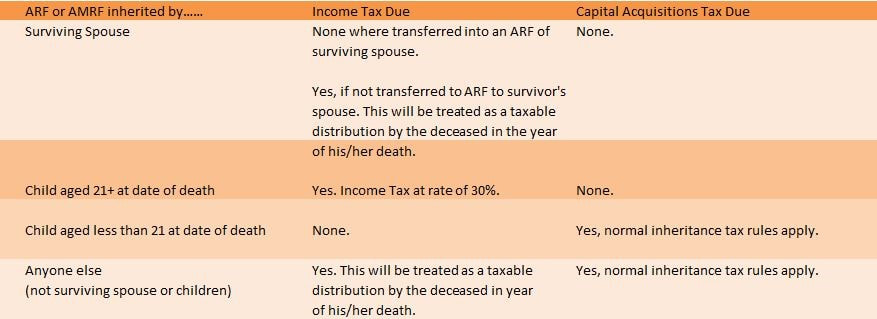

What happens to my ARF if I die?

On your death your ARF can be transferred tax-free to your spouse / civil partner who can continue to manage the ARF investments and take withdrawals. Alternatively your ARF can be left to your children or other persons, subject to income and / or inheritance tax.

How will these be taxed?

Financial Advice for Retirement Planning from a qualified Retirement Planning Adviser (RPA)

We all have ambitious plans to provide ourselves with a secure income in retirement. However, in order to make this a reality we need to put in place a financial plan. A pension remains the most tax efficient method of achieving this.

Retirement Planning for Company Director?

- Significant pension contributions can be made

- Tax free lump sum at retirement

- Potentially access your fund from age 50

Retirement Planning for Self Employed/Employees?

- Structure pension plans efficiently

- Contributions depend on age/earnings

- Retirement age 60-75

MOVING PENSION?

- Invest/Transfer existing pension assets

- Any growth within a retirement fund is exempt from tax

- Potentially access your fund from age 50

Personal Retirement Bond

A Personal Retirement Bond (also known as a Buy Out Bond) allows you to transfer your former company pension to a personally owned pension plan, to access at your retirement age. It puts you in control of your pension assets.

Where you hold a pension in a former employer’s defined benefit pension scheme, there are a number of factors to consider before making a decision to transfer your funds to a new employer’s scheme or to a Personal Retirement Bond. You should talk to your

Financial Broker about the pros and cons of transferring now or waiting to get the pension from the scheme when you retire

Where you hold a pension in a former employer’s defined benefit pension scheme, there are a number of factors to consider before making a decision to transfer your funds to a new employer’s scheme or to a Personal Retirement Bond. You should talk to your

Financial Broker about the pros and cons of transferring now or waiting to get the pension from the scheme when you retire

Who can set up a Personal Retirement Bond (PRB)?

- Anyone leaving or already left an employment with a pension fund relating to that employment.

- Anyone leaving their occupational pension scheme.

- Anyone whose company pension scheme is being wound up

What are the Benefits of a Personal Retirement Bond (PRB)?

- You have control over where your funds are invested. You can invest in Property, Funds, Shares and Bank Deposits.

- You can access the fund from age 50 (subject to certain conditions).

- You have control over the cost of your fund.

How can I access the funds from my Personal Retirement Bond?

Depending on the type of pension scheme from which the transfer value paid into your Buy Out Bond came from, you will have a number of options when it comes to taking your retirement benefits:

Remember: You can draw on your Buy Out Bond from age 50 onwards. If you become seriously ill before the age of 50, you may be able to draw on your Buy Out Bond immediately.

Your Financial Broker will be able to explain how you can access your Buy Out Bond benefits when the time comes.

- You may be able to take part of the fund as a lump sum

- You may be able to use the balance to buy an annuity, or

- You may be able to transfer the balance to a mix of an Approved Retirement Fund (ARF) and an Approved Minimum Retirement Fund (AMRF) in your own name. This depends on whether the pension scheme, you took the transfer value from, provided this option to you at the time of transfer to your Personal Retirement Bond.

Remember: You can draw on your Buy Out Bond from age 50 onwards. If you become seriously ill before the age of 50, you may be able to draw on your Buy Out Bond immediately.

Your Financial Broker will be able to explain how you can access your Buy Out Bond benefits when the time comes.